32

How to automate financial data collection and storage in CrateDB with Python and pandas

In this step-by-step post, I introduce a method to get financial data from stock companies. Then, I show how to store this data in CrateDB and keep it up to date with companies’ data.

This tutorial will teach you how to automatically collect historical data from S&P-500 companies and store it all in CrateDB using the Python language.

tl;dr: I will go through how to

import S&P-500 companies’ data with the Yahoo! Finance API into a Jupyter Notebook

setup a connection to CrateDB with Python

create functions to create tables, insert values, and retrieve data from CrateDB

upload finance market data into CrateDB

Before anything else, I must make sure I have my setup ready.

So, let’s get started.

CrateDB is a robust distributed SQL database and makes it simple to ingest and analyze massive amounts of data in real-time, making it perfect for this project.

To connect to CrateDB for the first time, I follow this step-by-step CrateDB installation tutorial, which has this and more methods to install CrateDB.

With the Ad-Hoc method, I first download CrateDB (version 4.6.1) and unpack it.

I then navigate in my terminal to the unpacked CrateDB root folder with the command

and run a single-node instance from CrateDB with

cd /crate-4.6.1 and run a single-node instance from CrateDB with

./bin/crate.Now I connect to the CrateDB Admin UI from my browser at http://localhost:4200

With CrateDB up and running, I can now make sure Python is set up.

The Python language is a good fit for this project: it’s simple, highly readable, and has valuable analytics libraries for free.

I download Python’s latest version, then reaccess the terminal to check if Python was installed and which version I have with the command

which tells me I have Python 3.9 installed.

pip3 --version, which tells me I have Python 3.9 installed.

All set!

The Jupyter Notebook is an open-source web application where one can create and share documents that contain live code, equations, visualizations, and narrative text.

A Jupyter Notebook is an excellent environment for this project. It contains both executable documents (the code) and human-readable documents (tables, figures, etc.) in the same place!

I follow the Jupiter Installation tutorial for the Notebook, which is quickly done with Python and the terminal command

and now I run the Notebook with the command

pip3 install notebookand now I run the Notebook with the command

jupyter notebookSetup done!

Now I can access my Jupyter Notebook by opening the URL printed in the terminal after running this last command. In my case, it is at http://localhost:8888/

On Jupyter’s main page, I navigate to the New button on the top right and select Python 3 (ipykernel)

An empty notebook opens.

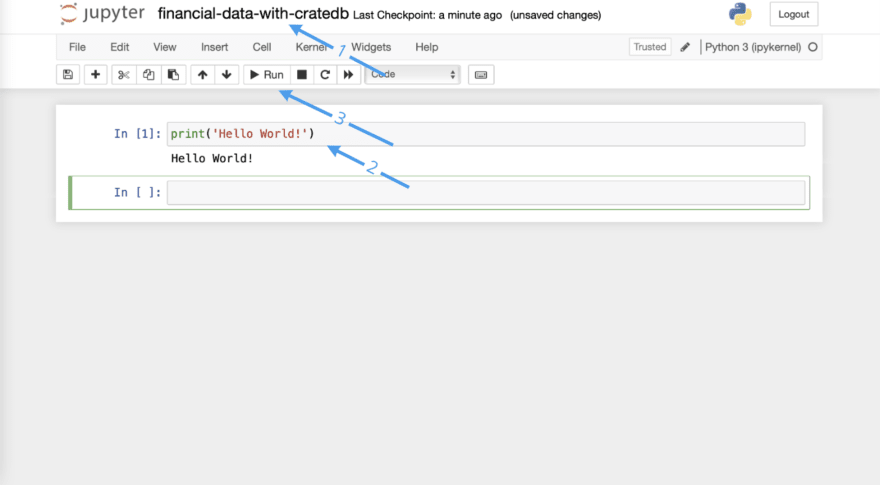

To make sure everything works before starting my project, I

print('Hello World!')Alt + Enter (or clicking on the Run button)

Great, it works! Now I can head to the following steps to download the financial data.

When I read yfinance's documentation, I find the

download function, which gets either a ticker symbol or a list of those as a parameter and downloads the data from these companies. As I want to download data from all S&P-500 companies at once, having a list with all their symbols would be perfect.

I then found this tutorial by Edoardo Romani, which shows how to get the symbols from the List of S&P-500 companies Wikipedia page and store them in a list.

So, in my Notebook, I import BeautifulSoup and requests to pull out HTML files from Wikipedia and create the following function:

import requests

from bs4 import BeautifulSoup

def get_sp500_ticker_symbols():

# getting html from SP500 Companies List wikipedia page

url = "https://en.wikipedia.org/wiki/List_of_S%26P_500_companies"

r = requests.get(url,timeout = 2.5)

r_html = r.text

soup = BeautifulSoup(r_html, 'html.parser')

# getting rows from wikipedia's table

components_table = soup.find_all(id = "constituents")

data_rows = components_table[0].find("tbody").find_all("tr")[1:]

# extracting ticker symbols from the data rows

tickers = []

for row in range(len(data_rows)):

stock = list(filter(None, data_rows[row].text.split("\n")))

symbol = stock[0]

if (symbol.find('.') != -1):

symbol = symbol.replace('.', '-')

tickers.append(symbol)

tickers.sort()

return tickersWhat this function does is:

data_rows variabledata_rows into the stock list, where each element of the list contains information about one stock (Symbol, Security, SEC filings, …)stock list element and adds it to the tickers list tickers list in alphabetical order and returns itTo check if it works, I will call this function and print the results with

tickers = get_sp500_ticker_symbols()

print(tickers)and it looks like this:

Now that I have a list of all the stock tickers, I can move on and download their data with

yfinance.Its key data structure is called a DataFrame, which allows storage and manipulation of tabular data: in this case, the columns are going to be the financial variables (such as “date”, “ticker”, “adjusted closing price”…) and the rows are going to be filled with data about the S&P-500 companies.

So, the first thing I do is import the yfinance and pandas

import yfinance as yf

import pandas as pdAnd now, I design a function to download the data from my list of companies.

Looking again at the documentation for yfinance, I see that the

download function returns a pandas.DataFrame object containing different kinds of information for a company, such as Date (which is the index for the DataFrame), Adjusted Close, High, Low, among others. I am interested in the Date and the Adjusted Close value, so I will extract the ‘Adj Close’ column from the DataFrame, as the index already includes the Date.

Apart from that, I only want to download data from a certain date on. Then, the next time I run this script, I can make sure only new data is being downloaded!

With that in mind, I create the

download_YFinance_data function:def download_YFinance_data(last_date):

tickers = get_sp500_ticker_symbols()

# downloading data from yfinance

data = yf.download(tickers, start = last_date)['Adj Close']

data.index.names = ['closing_date']

data.reset_index(inplace = True)

return dataAt the end of this function, I rename the index (which contains the date) to ‘closing_date’, as this is the column name I prefer for CrateDB, and then I reset the index.

Now, instead of having the date as the index, I have a column called ‘closing_date’, which has the date information, and the rows are indexed trivially (like 0, 1, 2, …). This will make it easier to iterate over the DataFrame in the next steps.

To check if everything works, I execute the function and store it in the

my_data variable, and print the result:my_data = download_YFinance_data('2021-11-16')

print(my_data)and it looks like this:

Great, now that I have my data set, I move on to connecting to CrateDB and creating functions to insert this data into my database.

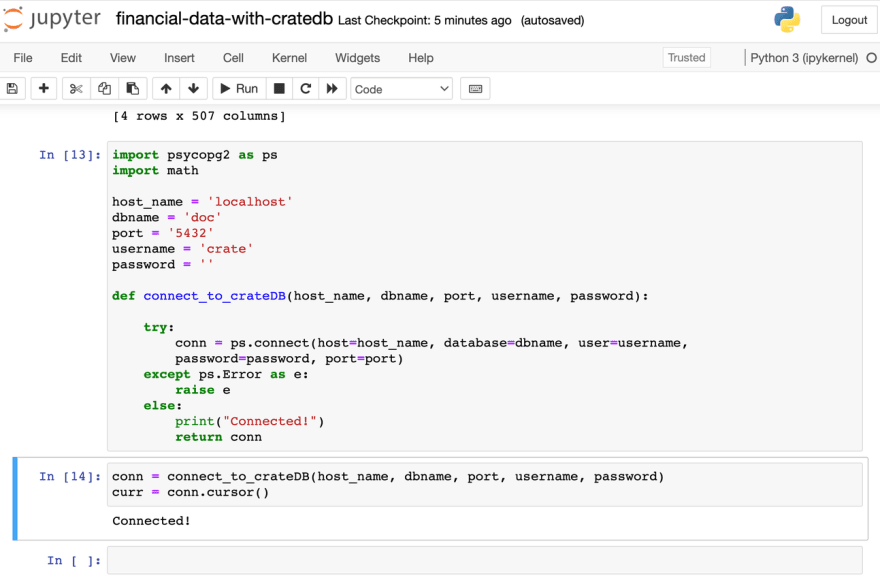

As CrateDB is highly compatible with PostgreSQL, I can use a PostgreSQL connector to connect to my database. The one I chose is psycopg2 , so I first install it with

import psycopg2 as ps

import mathand I also import the

math package, which will be necessary for further steps. I set the connection credentials as variables and create a function to connect to CrateDB using psycopg’s

connect function:host_name = 'localhost'

dbname = 'doc'

port = '5432'

username = 'crate'

password = ''

def connect_to_crateDB(host_name, dbname, port, username, password):

try:

conn = ps.connect(host = host_name, database = dbname, user = username,

password = password, port = port)

except ps.Error as e:

raise e

else:

print("Connected!")

return conn5432 is the standard port when connecting to CrateDB using PostgreSQL, and I can log in with the standard crate user, which has no password.

I create a

conn variable, which stores the connection, and a curr cursor variable, which allows Python code to execute PostgreSQL commands.conn = connect_to_crateDB(host_name, dbname, port, username, password)

curr = conn.cursor()When I run this code, ‘Connected!’ is printed, which means I have successfully connected to CrateDB.

Now I can create more functions to create tables in CrateDB, insert my data values into a table, and retrieve data!

In my table, I will have the closing_date, ticker and adjusted_close columns. Also, I want to give the table name as a parameter, and only create a new table in case the table does not exist yet. That’s why I use the SQL keywords

CREATE TABLE IF NOT EXISTS in my function.Now I need to create the complete statement as a string and execute it with the

curr.execute command:def create_table(table_name):

columns = "(closing_date TIMESTAMP, ticker TEXT, adjusted_close FLOAT)"

statement = "CREATE TABLE IF NOT EXISTS \"" + table_name + "\"" + columns + ";"

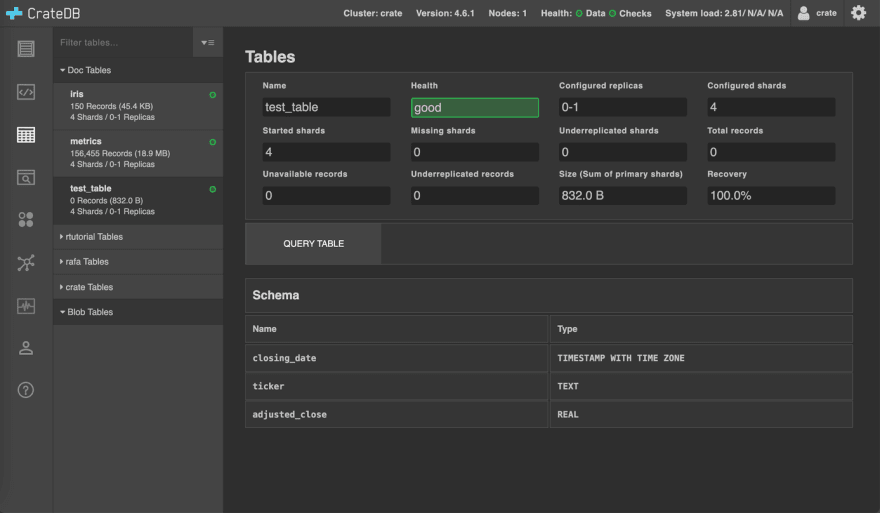

curr.execute(statement)I check if it works by creating a new test_table and then heading to the CrateDB Admin UI to see if my function created a table.

create_table('test_table')

And in fact, I can see the new (empty) table in the CrateBD Admin UI!

Note: the iris and metrics tables, as well as the other database schemas such as rtutorial and crate are not related to this tutorial. By following it step by step, one would only see the new test_table in the doc schema

Now I can move on to creating an insert function.

I want to create a function that:

(In the next steps I go through each part of this function. However, I have a snippet of the complete function at the end of this section)

Formatting the entries is crucial for successful insertion.

However, because of that, this function became rather long: so I will go through each section separately and then join them all in the end.

df: that way I can edit the DataFrame without changing the original data. Then, I create a table with the table_name (a new table will only be created in case there is no table with such a name). Finally, I create a ticker_symbols variable, which stores the list of company symbols.

def insert_values(table_name, data):

df = data.copy()

# creates a new table (in case it does not exist yet)

create_table(table_name)

ticker_symbols = get_sp500_ticker_symbols()df so that it matches a supported type, in this case, timestamp (without time zone).

# formatting date entries to match timestamp format

df['closing_date'] = df['closing_date'].astype('|S')

for i in range(len(df['closing_date'])):

df['closing_date'][i] = "'{}'".format(df['closing_date'][i] + "{time}".format(time = "T00:00:00Z"))df and store it as a list in date_values, create the first part of the insert statement in insert_stmt and create an empty array values_array, where I will keep the value tuples for each company on that date. (closing_date, ticker, adjusted_close) tuple for each company and adds it to my values_array. values_array to my insert_stmt and separate all tuples with commas to match the statement standards.curr.execute(insert_stmt)

# formatting data to fit into insert statement and creating statement

for i in range(len(df)):

# saving entries from the ith line as a list of date values

date_values = df.iloc[i, :]

# first part of the insert statement

insert_stmt = "INSERT INTO \"{}\" (closing_date, ticker, adjusted_close) VALUES ".format(table_name)

# creating array of value tuples, as [(c1, c2, c3), (c4, c5, c6), ...]

values_array = []

for k in range(len(ticker_symbols)):

ticker = ticker_symbols[k]

# the date is always the first value in a row

closing_date = date_values[0]

# index is [k+1] because the date itself is in the first position ([0]), so all values are shifted

adj_close = date_values[k+1]

# checking if there is a NaN entry and setting it to -1

if (math.isnan(adj_close)):

adj_close = -1;

# putting a comma between tuples, but not on the last tuple

values_array.append("({},\'{}\',{})".format(closing_date, ticker, adj_close))

insert_stmt += ", ".join(values_array) + ";"

print(insert_stmt)

curr.execute(insert_stmt)I test this function by running

insert_values('test_table', my_data)And it works!

And here is the complete

insert_values function:def insert_values(table_name, data):

df = data.copy()

# creates a new table (in case it does not exist yet)

create_table(table_name)

ticker_symbols = get_sp500_ticker_symbols()

# formatting date entries to match timestamp format

df['closing_date'] = df['closing_date'].astype('|S')

for i in range(len(df['closing_date'])):

df['closing_date'][i] = "'{}'".format(df['closing_date'][i] + "{time}".format(time = "T00:00:00Z"))

# formatting data to fit into insert statement and creating statement

for i in range(len(df)):

# saving entries from the ith line as a list of date values

date_values = df.iloc[i, :]

# first part of the insert statement

insert_stmt = "INSERT INTO \"{}\" (closing_date, ticker, adjusted_close) VALUES ".format(table_name)

# creating array of value tuples, as [(c1, c2, c3), (c4, c5, c6), ...]

values_array = []

for k in range(len(ticker_symbols)):

ticker = ticker_symbols[k]

# the date is always the first value in a row

closing_date = date_values[0]

# index is [k+1] because the date itself is in the first position ([0]), so all values are shifted

adj_close = date_values[k+1]

# checking if there is a NaN entry and setting it to -1

if (math.isnan(adj_close)):

adj_close = -1;

# putting a comma between values tuples, but not on the last tuple

values_array.append("({},\'{}\',{})".format(closing_date, ticker, adj_close))

insert_stmt += ", ".join(values_array) + ";"

curr.execute(insert_stmt)Now I can move on to the last function, which is quite handy regarding the automation.

I want my stock market data in CrateDB to be up to date, which requires that I run this script regularly.

However, I do not want to download data I already have nor have duplicate entries in CrateDB.

That’s why I decide to create this function, which selects the most recent date from the data I have in my CrateDB table. Then, I give this date as a parameter in the

download_YFinance_data function: this way, this function will only download new data!def select_last_inserted_date(table_name):

# creating table (only in case it does not exist yet)

create_table(table_name)

# selecting the maximum date in my table

statement = "select max(closing_date) from " + table_name + ";"

curr.execute(statement)

# fetching the results from the query

recent_date = curr.fetchall()

# if the query is empty or the date is None, start by 2015/01/01

if (len(recent_date) == 0 or recent_date[0][0] is None):

print("No data yet, will return: 2015-01-01")

return "2015-01-01"

# format date from timestamp to YYYY-MM-DD

last_date = recent_date[0][0].strftime("%Y-%m-%d")

# printing the last date

print("Most recent data on CrateDB from: " + last_date)

return last_dateI can test this function by running

select_last_inserted_date('test_table')

And now everything is set!

I have all the necessary functions ready to work!

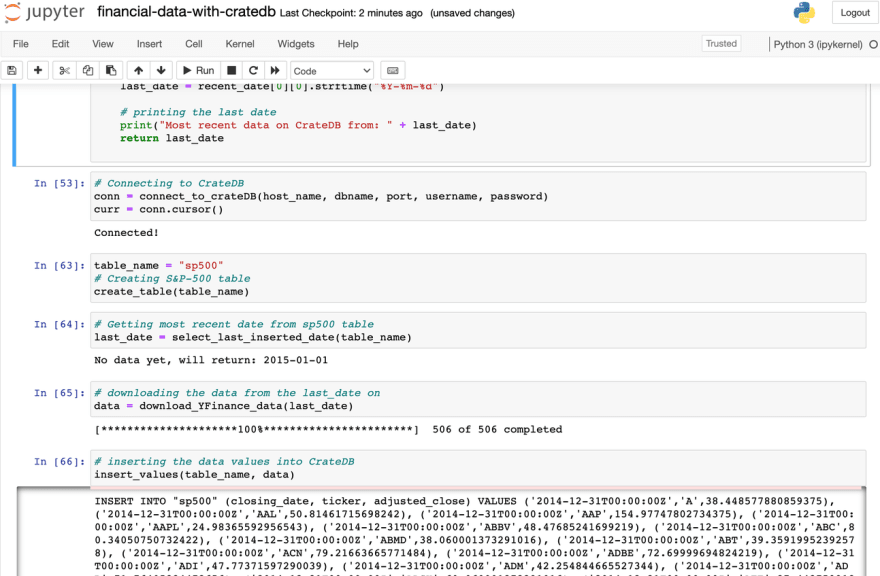

To have a clean final test, I

These new calls look like this:

# Connecting to CrateDB

conn = connect_to_crateDB(host_name, dbname, port, username, password)

curr = conn.cursor()

table_name = "sp500"

# Creating S&P-500 table

create_table(table_name)

# Getting most recent date from sp500 table

last_date = select_last_inserted_date(table_name)

# downloading the data from the last_date on

data = download_YFinance_data(last_date)

# inserting the data values into CrateDB

insert_values(table_name, data)

I navigate to the CrateDB Admin UI, where I see the new table sp500 was created and that it is filled with the financial data

I make a simple query to get Apple’s data from my sp500 table

select *

from sp500

where ticker = 'AAPL'

order by closing_date limit 100;And instantly get the results

Now I can profit from CrateDB’s speed to query over 77k financial records and run this script whenever I want to update my database with new data!

In this post, I introduced a method to download financial data from Yahoo Finance using Python and pandas and showed how to insert this data in CrateDB.

I profited from CrateDB’s high efficiency to rapidly insert a large amount of data into my database and presented a method to get the most recent input date from CrateDB. That way, I can efficiently keep my records in CrateDB up to date!

32